(a)

The expenditure approach can be used to determine the national income in the 4-sector open economy of Singapore. This requires consideration of the circular flow of income.

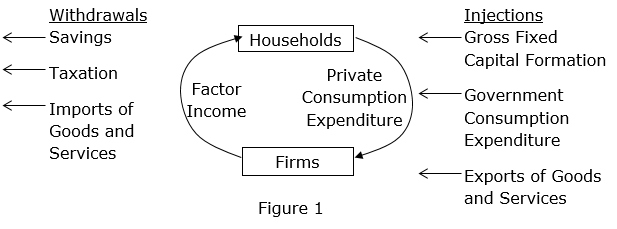

The circular flow of income is a representation of the flow of money and goods and services between economic agents. The 4-sector open economy of Singapore comprises of households, firms, government and the rest of the world.

With reference to Figure 1, households will supply their factors of production to firms in return for factor income. Firms will produce supply goods and services with the factors of production, part of it going to the households in exchange of private consumption expenditure with the rest going to the international market for export revenue. Firms also invest in new plant and machinery. Beyond consumption expenditure, some of their income are saved, taxed, and spent on imported goods and services. The government’s consumption expenditure will go to both households and firms in terms of grants and subsidies.

Based on the circular flow of income, the national income in Singapore can be determined by the aggregate expenditure of the economy. This is the summation of private consumption expenditure, gross fixed capital formation, government consumption expenditure, and net exports of goods and services, i.e. $(129 + 77 + 34 + 531 – 444) billion = $327 billion. Singapore’s national income is most heavily dependent on the rest of the world. Total trade stands at a massive 298% of GDP. This is due to Singapore’s small market due to small population size. As such, firms cannot depend only on household’s private consumption for survival, which takes up a relatively small 39.4% of GDP. Hence, firms look to the international market in order to increase their revenue. Moreover, Singapore is also very dependent on imports due to her lack of raw materials. In Singapore, government consumption constitutes only a small proportion of GDP, at only 10.4%. This is because the government practices fiscal prudence during times of economic prosperity to build up reserves in preparation for possible future crisis. It is important that the government do not overspend during times of economic boom and be in constant fiscal deficit. Otherwise, it may not have sufficient resources to respond to a crisis. Firm’s investment level is also relatively low at 23.5% of GDP. While not comprising a significant portion of GDP, investment is crucial for Singapore to remain competitive and continuously expand her productive capacity, potentially affecting future national income. In conclusion, the most important of the key sectors of the circular flow of income in determining the national income in Singapore would be the rest of the world. As a small and open economy without natural resources, trade is vital to the growth of Singapore and her national income. While comparatively more important than the other sectors, the trade sector may suffer during a global recession. During this period, household and government will be crucial in cushioning the impact of a fall in trade. Moreover, investment will ensure Singapore’s trade sector remain competitive in the international arena. (b)

Exchange rate of Singapore dollar (SGD) measures the price of SGD in terms of foreign currencies. An appreciation of the Singapore dollar (SGD) refers to the increase in the value of the SGD relative to other foreign currencies. This is due to changes to the forces of demand and supply of SGD. The gain in value of the SGD will have impact on both Singapore’s national income and its components.

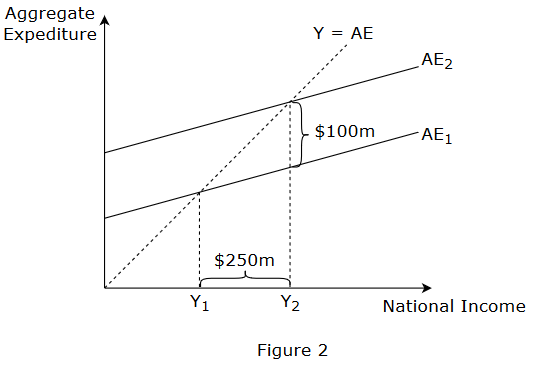

When Singapore’s exchange rate appreciates, imports will be relatively cheaper in terms of local currency. Assuming that the demand for imports is price inelastic, since Singapore is dependent on imports for foodstuff and raw material, this will lead to a less than proportionate increase in the quantity demanded. As such, the increase in expenditure from the increase in quantity demanded will be lesser than the decrease in expenditure from the decrease in price. Hence, import expenditure will decrease. On the other hand, due to appreciation, exports will become relatively more expensive in terms of foreign currency. However, this is partially offset by the lower price of exports due to lowered cost of production as import expenditure decrease. Assuming that the demand for exports is price elastic due to the availability of substitutes, this will lead to a more than proportionate decrease in quantity demanded. As such, export revenue will fall. However, the decrease is not expected to be larger than the fall in import expenditure as the overall price increase for exports is less substantial. Hence, net exports will likely increase. With an appreciation leading to price of imports being relatively cheaper in terms of local currency, this will decrease the demand for local products as households switch from purchasing local products to imports assuming substitutes are available. As such, private consumption expenditure is expected to fall. However, this fall is not expected to be significant since the increase in quantity demanded for imports is minimal as demand for imports is price inelastic. Investment is also likely to increase as an appreciation of the Singapore currency will lead to higher business confidence since it signifies a stronger economy and generates positive business outlook. This will cause firms to revise upwards their expectations of future profits due to optimism about the demand for their goods. Investment will thus increase. However, this increase is unlikely to be substantial given that appreciation leads to investment becoming more costly and also reduces the attractiveness to invest as it reduces export price competitiveness. As the increase in net export and investment is likely to outweigh the minimal decrease in consumption, aggregate expenditure will increase. This will lead to a multiple increase in Singapore’s national income via the multiplier effect if the economy is below full employment. Assuming that aggregate expenditure increases by $100m, this will lead to an increase in the production of output and income by $100m in the round one effect because an equivalent amount will be paid to the owners of the factors of production in the form of wages, interest, rent, and profits. Taking the marginal propensity to withdraw (mpw) as 0.4, which includes the marginal propensity to save (mps), marginal propensity to tax (mpt), and marginal propensity to import (mpm), $40m will be saved, taxed, and leaked out as imports. Households will spend 60% of the additional income ($60m) on consumer goods in period two. Consumer goods industry will experience an increase in demand and will thus have to expand production. Additional factors of production will have to be employed, and are in turn paid a total of $60m. Resource owners will spend $36m, with the rest being withdrawn from the circular flow of income. This process of alternating and income generation will go on until there is no more additional spending. Ultimately, the increase in income is $250m as the multiplier is 2.5 (k = 1/mpw).

With reference to figure 2 above, an increase in aggregate expenditure by $100m from AE1 to AE2 will lead to a multiple increase in national income from Y1 to Y2 by $250m via the multiplier process.

In Singapore, the increase in national income is not expected to be large due to the small multiplier. Singapore has a high mps due to due to her compulsory savings scheme, Central Provident Fund, and high mpm due to her dependency on imports. If the economy is near or at full employment, an increase in AE will have limited or no impact on national income respectively but leads to inflationary pressures instead, due to higher cost of production caused by resources getting scarcer. However, the above analysis rests on the underlying assumption that the global economy is enjoying an economic expansion. If there is a global recession, appreciation may generate an opposite impact on the Singapore’s economy. Export revenue is expected to fall sharply due to a combination of a reduction in global purchasing power and loss of price competitiveness. This will likely outweigh the fall in import revenue, leading to an overall decrease in net export. Furthermore, with a pessimistic business outlook and fall in business confidence due to the global recession, firms will revise downwards the expected return of projects and cancel unprofitable investment projects. Coupled with the loss in price competitiveness of exports, investment is expected to decrease largely. Hence, appreciation during an economic downturn will cause a fall in consumption, investment, and net exports in Singapore. While it is expected that the government will increase her expenditure in order to stimulate the economy, it is unlikely that this increase can offset the combined decrease in the above mentioned factors. Hence, aggregate expenditure will decrease, leading to a multiple decrease in national income via the multiplier effect. In conclusion, the likely effects on Singapore’s national income and its components when its exchange rate appreciates are largely dependent on the state of the economy. Investment and net exports is expected to increase during times of economic boom and fall during a global recession while consumption is expected to decrease for both scenarios. In both cases, government expenditure is unlikely to be affected by an appreciation as it is autonomous. Also, the change in national income will not be significant due to Singapore’s small multiplier. |

|