(a) (i)The data in Table 3 supports the suggestion as UK experienced a relatively larger negative GDP growth rates in 2008 and 2009 compared to other major economies and is slow in recovery in 2010 and 2011 with a relatively lower GDP growth rates.

The exception to the above is France and Japan which appears to be doing as poorly as UK. (a) (ii)Both Japan and Singapore have displayed higher GDP growth rates in 2010 and 2011 compared to 2008 and 2009.

However, Japan generally experienced negative growth rates over the period from 2008 to 2011 while Singapore generally experienced positive growth rates over the same period. (b)In all economies, there exists the problem of scarcity as the unlimited wants cannot be satisfied by the limited resources available. Therefore, it is inevitable to choose how to allocate resources to satisfy some wants and forgo others. This incurs opportunity cost, which is the next best alterative forgone in making a choice.

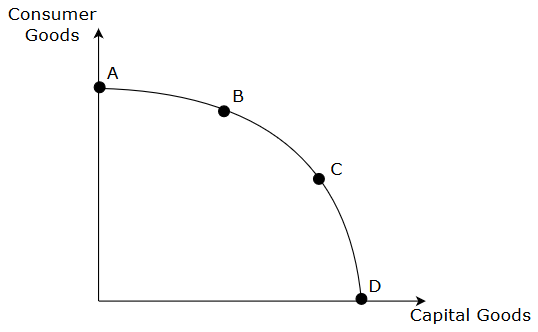

The same applies equally for an economy deciding to allocate resources between capital and consumer goods, given the limited amount of resources available. A high level of investment will correspond to the production of more capital goods. As more resources are dedicated to producing capital goods, fewer resources will be channelled to produce consumer goods, as illustrated in the production possibility curve below.

As the production of capital goods increases, due to high level of investment, the production point will shift towards D from A. This will reduce the amount of capital goods produced. In this case, the opportunity cost of high level of investment to produce capital goods is consumer goods.

Hence, despite the likelihood that a high level of investment will generate potential growth, consumers’ are worse off in the short run as they will have to sacrifice on their consumer goods consumption. This can lead to lowered standard of living and makes high level of investment undesirable. (c) (i)The four elements identified in Extract 8 are consumers spending, government capital spending, export revenue, and investment.

(c) (ii)As mentioned in Extract 8, the ‘Keynesian option’ refers to planning for a budget deficit by reducing taxation and increasing government spending in order to achieve economic growth. This is also known as the expansionary fiscal policy.

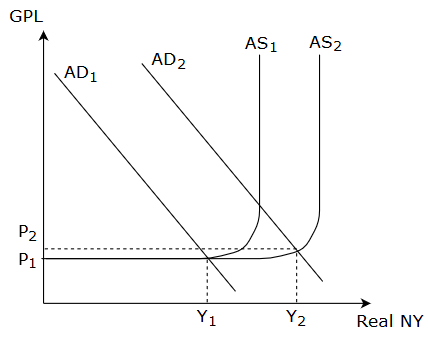

The government can reduce tax rates to stimulate consumption (C) and investment (I). By reducing personal income tax, consumers’ spending (consumption) will increase due to an increase in disposable income and purchasing power. Indirect taxation on good and services can also be reduced to increase consumption as this will enable a given disposable income to purchase more goods and services. Furthermore, by reducing corporate tax rates leading to increase in after-tax profits, private investment will be encouraged. To increase government expenditure (G), the government can increase its spending on public projects such as construction and improvement of the transport network, building more schools and improving hospital facilities. By increasing C, I, and G, three of the four elements identified in part (c) (i) is achieved. Aggregate demand (AD) will increase since AD = C + I + G + (X-M). Furthermore, the above can also have supply side effects as the quantity and quality of factors of productions are increased. This is due to increase in the country’s stock of capital as government develops infrastructure, increase in labour supply with income tax reduction, and improvement in productivity of workers and technological level due to increased research and development with corporate tax reduction. Hence, aggregate supply (AS) increases as the country’s productive capacity is increased, indicating that potential growth is achieved.

With reference to the diagram above, as AD increase from AD1 to AD2 and AS increase from AS1 to AS2, the real national income (NY) will increase from Y1 to Y2 via the multiplier effect, indicating that actual growth is achieved.

Hence, despite worsening public debt as identified in Extract 8, the economy will be able to achieve both actual and potential growth under the ‘Keynesian option’. (d)In order to spur economic growth, the UK government has lowered interest rates in order to encourage private investment (Extract 8). When interest rates decreases, some marginal projects become profitable due to lower cost of borrowing. As such, firms will increase their private investment.

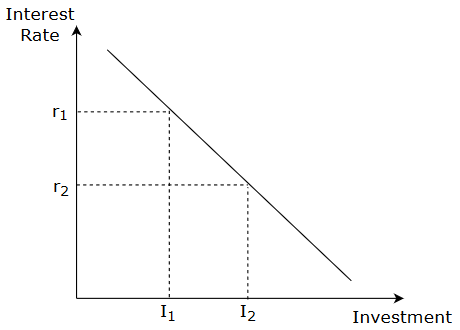

As illustrated in the diagram above, a fall in interest rate from r1 to r2 will increase the investment level in the economy from I1 to I2.

The effectiveness of lowering interest rates to increase private investment is largely dependent on two factors. Firstly, the more interest elastic the marginal efficiency of investment (MEI) curve of an economy is, the more successful lowered interest rates will be. The elasticity of MEI is dependent on whether interest rate is the main determinant of investment. When MEI is interest elastic, a fall in interest rates will lead to a more than proportionate increase in level of investment. This is in contrast to an interest inelastic MEI, whereby a fall in interest rates will only lead to a less than proportionate increase in level of investment. Secondly, business confidence will also affect the willingness of producers to increase investment. Producers will likely invest more in an economy with stronger growth and more positive outlook as they will be more confident of generating profits from their investment. Hence, lowered interest rates may not be suitable to achieve strong increase in investment level in a sluggish economy. In the case of UK, there seems to be little increase in investment despite lowered interest rates, according to Extract 8, due to MEI likely being interest inelastic and poor business confidence. Therefore, a struggling economy should not rely solely on lowered interest rates to increase the level of private investment as this policy is only most effective in a strong economy with high business confidence. In the case of a struggling economy, China’s approach of using large state-owned company and banks to increase investment directly (Extract 7) may be a more effective option. (e)According to Extract 8, UK is suffering from a recession and public sector deficit. A recession refers to at least two quarters of negative economic growth and public sector deficit refers to government expenditure being higher than tax revenue. It is crucial for the government to manage these two problems in order for the economy to recover and prevent any possible deterioration to the standard of living.

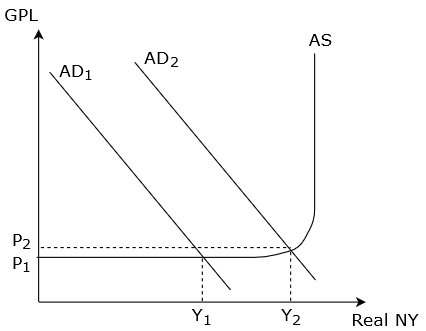

A possible solution is to opt for a fiscal policy that involves ‘more drastic cuts to public spending’. This refers to decreasing government expenditure, which can be done by reducing spending on civil servants salary, healthcare, and education, and delaying infrastructure development projects including buildings and roads. This reduction in government expenditure will thus be able to reduce the public sector deficit, assuming that tax revenue remains constant. With a healthier government budget, the government can thus reduce taxation in the private sector (Extract 8), including reduction in personal and corporate tax. As elaborated in part (c) (ii), this will lead to an increase in consumption and investment, which is compounded by increased confidence in the economy due to lower debt. This stimulates a private sector recovery which will spur economic growth. Assuming that the increase in consumption and investment is higher than the decrease in government expenditure, AD will ultimately increase according to the diagram below.

As AD increases from AD1 to AD2, real national income will increase by a multiple from Y1 to Y2. This will achieve actual growth, pulling the economy out of a recession.

However, the success of this policy is dependent on the private sector’s optimism about the economy. The reduction in tax rates will only generate substantial increase in consumption and investment only if consumers and producers have confidence in the economy. Furthermore, in order to reduce public debt effectively, the reduction in government expenditure will likely be more significant than the lowering of tax rates. This means that AD may in fact fall, contracting the economy and leading to negative growth as the decrease in government expenditure is larger than the increase in consumption and investment. Furthermore, people will have to suffer a lower standard of living as access to important goods such as health care and education is reduced with government’s cut in public spending and infrastructure development projects are halted. This is worse for civil servants who received reduction in their salary, leading to lower disposable income and hence purchasing power. Ultimately, there may even be a decrease in the productive capacity of the economy, with reduced productivity due to above mentioned reasons and decreased labour supply. With poor or negative economic growth, the government’s tax revenue will be limited, ultimately leading to a worsening public debt. In view of the above limitations, the government might want to consider alternatives. A possible way is to adopt the ‘Keynesian option’ (Extract 8) or otherwise known as the expansionary fiscal policy which may lead to both actual and potential growth as discussed in part (c) (i). This is useful for the country to generate economic growth to pull itself out of the recession and also build solid foundations for future developments. Furthermore, with strong economic growth accompanied by a fall in cyclical unemployment, government expenditure in terms of unemployment benefits can be reduced. With tax revenue collected increasing during economic growth, the government will be able to reduce its public sector deficit. However, the effectiveness of the ‘Keynesian option’ is limited by the financial crowding out effect. This is because the government tis already suffering from a budget deficit. In order to increase spending, the government will have to borrow in competition with the private sector for funds. This will increase the interest rates in the market. This increase in interest rate will offset the effect of a reduction in tax rates, leading to a lower than intended increase in consumption and investment. Hence, AD may only increase marginally. Moreover, government debt will worsen (Extract 8) in the short term as spending has to be increased with tax rates reduced, worsening the existing problem. Another alternative is to focus on export-led growth which has been successful for China’s economy (Extract 7). The government can attempt to increase export revenues via reduction of interest rate to encourage investment to raise productivity and devaluation of the currency. By reducing interest rate, producers will be able to increase their level of investment as some marginal projects become profitable. If the investment is channelled into research and development, producers may be able to improve the quality of their products or lower their cost of production with improved efficiency. This will make the exports both more price and non-price competitive in the international market, leading to an increased in export revenue. With devaluation, there will be a fall in the external value of the currency relative to its trading partners The reduction in interest rate can also lead to depreciation due to capital flight. This leads to the exports becoming relatively cheaper in terms of foreign currency and imports becoming relatively more expensive in terms of local currency. Assuming that the Marshall-Lerner condition is satisfied, export revenue will increase and import expenditure will fall. This will lead to an increase in net exports. As net exports increase, AD will increase leading to a multiple increase in national income and hence actual growth. This will pull the economy out of a recession. With growth, tax revenues can be increased with government expenditure decreases from reduction in unemployment benefits. However, the success of the above strategy will be limited if the global economy is weak (Extract 8). During a global financial crisis, most countries will be suffering from a recession, leading to a decrease in real national income and hence purchasing power. This will decrease the demand for exports. Furthermore, devaluation of the currency may lead to competitive devaluation as it affects trading partners adversely. This will reduce the effectiveness and extent of the increase in net exports. Also, it may reduce the confidence in the country’s currency if devaluation is carried out consistently or extensively. In conclusion, a government faced with recession and public sector debt should avoid opting for a fiscal policy that involves ‘more drastic cuts to public spending’ as it may worsen the problem and lower people’s standard of living. The government should instead consider adopting the ‘Keynesian option’ together with pursuing export-led growth in order for the economy to recover. While public debt will increase in the short run, foundations are built for future developments without worsening of public morale. |

|